With the first year of budgeting under the 3% cap in the rearview mirror, counties indicate while they may have been able to make ends meet for 2026, they are very concerned about future budget cycles. A tax reform package passed by lawmakers in the 2025 Legislative Session restricts political subdivisions by capping annual property tax increases to 3% each year. The North Dakota Association of Counties (NDACo) developed a survey for counties to complete with the goal of capturing the impacts of the restriction on county budgets. 51 of the 53 Counties responded. “This survey provides insight into how counties managed their 2026 budgets with the mandated limitations along with their outlook on how the 3% cap will impact the well-being of the county in the future,” said NDACo Government Relations Specialist Donnell Preskey during the Interim Tax Reform and Relief Advisory Committee meeting.

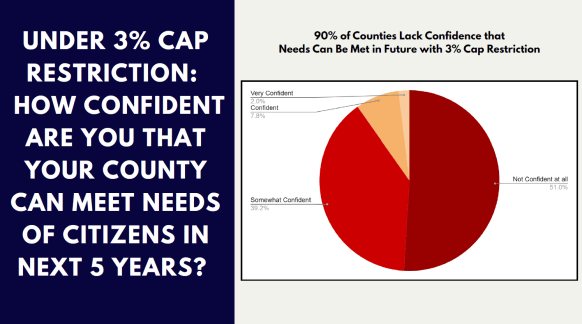

The survey highlights how a great majority, 90% of the counties, lack confidence that their county can meet the needs of citizens in the next five years. That’s because most counties tapped into their reserves to fund their 2026 budgets, which will deplete quickly in the cap environment. Counties reiterated that the use of reserves to fill the gap in budgets is unsustainable. In dollars, the allowed revenue calculated from the 3% cap limit varies significantly depending on the property tax base a county has. For example, in Slope County, the 3% cap equaled only $18,000 in revenue growth from property taxes compared to Cass County where the cap allowed an increase of $1.8 million.

The legislation allows counties to carry forward unused percentages of the 3% cap for up to five years. 34 Counties had a portion of the 3% that was unused, while 17 counties reported they used the full 3% allowed. Of those 17 counties, 13 of them also dipped into their reserves to fund their budgets.

Counties Make Budget Cuts

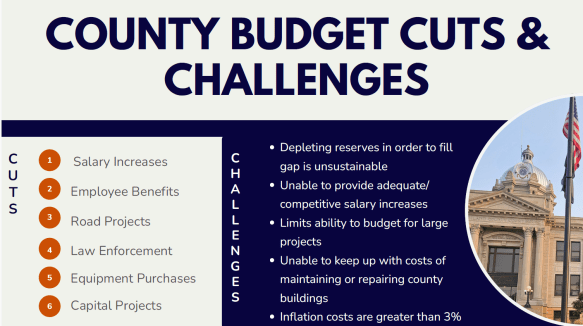

There are real fiscal impacts as a result of the property tax limitation. Numerous counties reported a loss in funding where levies are tied to state grants, with road funding seeing the greatest impact. Counties also reported that they were forced to defer equipment purchases. Overall, counties prepared their 2026 budgets to the best of their abilities, but the comments and results of the survey illustrate a bleak outlook for budgeting and planning in the future. Counties indicated they made budget cuts in several areas including: salary increases, employee retirement benefits, road projects, equipment purchases and capital projects. These cuts highlight challenges counties see as they prepare for the next budget cycle and into the future. These challenges include depleting reserves, being unable to provide adequate and competitive salary increases, putting off large projects including maintaining or repairing county buildings. The financial pressures are only compounded by the fact that counties experience inflation costs greater than 3%.

The legislation allows local governments to exceed the 3% cap if voters approve it in the general election. NDACo is not aware of any counties bringing this issue to their voters in 2026.

NDACo Offers Future Considerations

NDACo offered a list of future considerations for lawmakers as they prepare for the 2027-28 Legislative Session. Many of the suggestions were related to expanding exemptions for the 3% cap. The primary exemption suggested is for health care premiums, as NDPERS is set by the state and saw a 15% increase in rates from the last biennium. Other suggested exemptions include elections, corrections, and unfunded state mandates. NDACo also brought to lawmakers’ attention that under current law, prior voter approved levies are subject to the 3% cap, something that may have been an oversight. Other proposals NDACo highlighted were adjusting the 3% cap either to reflect inflation or to a higher percentage, creating a public safety levy authority, eliminating current mill rate limitations, providing a state appropriation for programming costs associated with tax statement requirements and providing additional state revenue sharing.

NDACo also flagged for the committee a list of technical items that should be addressed next session that have been identified by counties when implementing HB 1176, the property tax relief and reform legislation.

Several other local government associations provided similar testimonies to the committee including the League of Cities, School Boards Association and the Township Officers Association.